We live in a digital age where every aspect of people’s personal and professional lives is increasingly conducted in the cloud. Companies and employees alike are adapting to and taking advantage of new possibilities for remote working, continuous communication, and other technology to fuel creativity and collaboration. But this same technology can make just as big an impact on your business’s healthcare costs. Businesses are used to the idea that meetings do not have to be conducted in person, and more and more are discovering that many medical visits do not, either.

The percentage of employers who offer a telemedicine program has doubled since 2015, according to a Mercer survey. That’s because it’s an effective strategy to reduce healthcare costs by encouraging employees to get treatment that heads off future healthcare expenses while preventing unnecessary doctor’s office, urgent care, and ER visits. In fact, the average savings per single employee annually is $300 according to the AMA, and that number goes up to $1000 per year for a family of four. Given that benefits like healthcare makeup 25-40% of most companies’ payroll expenses, tackling healthcare expenses through telehealth seems like a worthwhile investment for any growing business. Especially since it is easy to implement and requires minimal upfront investment.

Best of all, implementing telehealth is a cost-cutting measure that actually increases the standard of care for your employees. That means that they are happier and healthier, making them more productive and engaged team members. So telehealth can boost your revenue and help you maintain a stable workforce while it reduces your healthcare costs.

So how exactly does telehealth generate savings which can help give SMBs the financial stability they need to grow? In this article we will explore how telehealth generates:

• Short-term savings from reduced cost of care

• Increased revenue due to employee performance

• Long-term savings

Reduced Cost of Care Generates Short-Term Savings

The clearest cost-cutting benefit to implementing telehealth is that employees will opt to get their medical advice digitally instead of by going to a doctor’s office, urgent care, or ER. These savings can add up quickly as telehealth consultations cost an average of $40, compared to $125 for equivalent office visits. So not only will your healthcare costs go down, but your employees’ out-of-pocket costs will too.

The biggest savings come from averted emergency room visits. Telehealth is highly effective in staving off these extremely expensive visits when employees have unexpected healthcare needs. A study of a telemedicine platform in Pennsylvania found that the majority of employee health concerns were resolved in a single virtual-consultation and that the telemedicine option generated short-term savings by diverting patients from higher-cost options. Each avoided emergency room visit saved $300-$1500, which can make a significant impact on growing businesses worried about maintaining their bottom line.

Telehealth provides employees with a convenient and affordable alternative to a wide range of traditional healthcare services that can incur significant healthcare expenses. That means that implementing a telehealth platform reduces short-term costs for employers and employees alike. It also means that employers will be able to negotiate lower premiums because their employees present a lower risk for insurers.

Increased Revenue from Employee Performance

The savings from diverting employees away from high-cost consultation and treatment options might be exceeded by the revenue generated from fostering a healthier and more engaged workforce. Making healthcare more accessible and affordable for your employees means that they will take advantage of it more often and receive the treatment that they need, making them more high-performing team members. Also, because telehealth can be accessed immediately and from anywhere, employees will not have to choose between going to work and getting medical advice. As a result, employers who implement a home telehealth platform can expect their employees to take fewer sick days due to doctor’s appointments.

Reducing absenteeism generates significant cost savings from increased worker productivity by itself, but it is just the tip of the iceberg. Healthier employees are more productive, straight and simple and telemedicine can help keep them that way. In the current employment and healthcare climate, employees frequently avoid treatment until an illness gets “bad enough”; which means that they come into work sick for extended periods. That’s bad news for companies because sick team members are less productive while collecting the same salary and benefits, and worse still can infect other employees. Getting treatment as soon as issues arise ensures that employees get back to peak performance as quickly as possible.

Home telehealth also streamlines the healthcare experience for employees and saves them significant time and money. That doesn’t just make them healthy and able to work but also makes them happier and more satisfied with their work. It is an additional benefit which makes your employees feel well taken care of, increasing their loyalty and their engagement with your company. Growing businesses can struggle to compete with larger companies to attract, engage, and retain the talent they need to succeed partially because their smaller budget limits the range of benefits that they can offer. Telehealth is a great way for these businesses to stand out for their meaningful benefits program while simultaneously reducing costs.

Long Term Savings

Home telehealth is not just about getting treatment when illness strikes: it also makes it easier to access preventive care and ongoing treatment for chronic conditions. As such, it can prevent significant future healthcare expenses from treating preventable or neglected conditions.

Employees are increasingly foregoing primary care visits and other preventive services. The total number of trips to primary care doctors dropped by 18% between 2012 and 2016. This issue is particularly great among Millennials, a third of whom do not even have a primary care doctor. That can become a big problem for employers as Millennials continue to make up a larger percentage of the workforce. Primary care can help identify potential issues before they become costly and damaging to the patient and provide holistic guidance that increases overall health. Telehealth can help fill in this gap, especially for tech-savvy Millennials.

Telehealth can also provide easy and affordable access to wellness benefits by helping to identify risk factors and guide employees through prevention. This matters because 70% of employer healthcare expenses come from preventable lifestyle-related conditions such as diabetes, heart disease, and lung cancer. Telemedicine consultations can help employees figure out what challenges they need to address and can help guide employees through the process of tackling those challenges. For example, telehealth platforms can give employees access to advice and consultation to support weight loss and smoking or alcohol cessation.

Using telehealth to manage treatment for chronic conditions can also lead to significant ongoing savings. People with chronic conditions account for three-quarters of doctor’s visits and nine out of ten prescriptions so managing their health effectively and cost-efficiently should be a priority for any employer. Telemedicine can make this care easier to get and cheaper for employee and company alike, reducing those doctor’s office visits and hospital stays. Employees can access advice about medication management quickly and easily while incurring fewer expenses for themselves and their employer. These savings can be especially great when combined with mail-order prescription fulfillment. And the long-term savings add up when you consider the significant healthcare expenses that can result from untreated, undertreated, or mistreated chronic conditions, all of which can result from under-utilization of healthcare options due to cost and inconvenience.

The last and frequently overlooked area in which telehealth can save your business money is in mental healthcare. Insurers, providers, and employers are beginning to recognize the importance of mental health in addition to physical health, but the infrastructure is still catching up to employee needs. Even when options are available, employees often avoid accessing mental healthcare because it is stigmatized and because regular psychologist or psychiatrist visits are too much of a hassle. Luckily, telemedicine has proven to be an effective method to treat mental health and is cost-effective for employers compared to in-person visits. Not only that, but it is more convenient and private than traditional treatment, making it more appealing to employees. That means that you can reduce employee burnout, underperformance, and turnover due to untreated mental conditions such as depression or anxiety. You will pay less for care and your employees will be happier and more engaged in their work, making them more valuable team members.

Key Takeaways

Home telehealth is a constantly expanding field and there is no way for us to cover every aspect of how it can improve your employees’ healthcare and your bottom-line in one article. But hopefully, we have given you a sense of how telehealth can play an essential role in your efforts to control healthcare costs. Just remember:

• Telehealth appointments are significantly cheaper than traditional alternatives and prevent costly ER and office visits

• The affordability and convenience of telehealth means that it can make your employees healthier and more productive, helping your business grow sustainably

• Telehealth can reduce ongoing and future healthcare expenses by supporting preventive care, managing treatment for chronic conditions, and providing mental healthcare

If you want to cut your business’s healthcare expenses while still attracting and retaining the talent you need to grow your business, telehealth should be just one part of your strategy. We will be hosting a comprehensive webinar to address how CFOs and business leaders can curb healthcare costs on September 19th at 11 AM CST. Learn from industry experts in benefits administration, telehealth, and more so that you can effectively manage your healthcare expenses. Register today!

Choosing a new health insurance broker to manage your employee benefits can be an overwhelming task. Health insurance and employee benefits are a large part of your payroll expenses, so picking your broker is a high-stakes affair. The quality of your new insurance broker can make the difference between having an engaged team of high-quality talent that fuels your growth or watching your best team members leave for employers who provide benefits which meet their needs.

In this article, we’ll take a comprehensive look at the process of choosing a new health insurance broker, including:

• Why your health insurance broker matters

• How to start the process to find a new health insurance broker

• What to look for in a new employee benefits broker

• How to tell if an insurance broker can really deliver value to your business

Why Your Health Insurance Broker Matters

Why is it so important to be strategic when it comes time to choose a new health insurance broker? Employee benefits, particularly healthcare, are enormously powerful tools in your arsenal to attract, retain, and engage the talent that you need to grow and sustain your business. Companies of all sizes are struggling to build and maintain effective teams as the job market encourages employees to switch jobs more frequently and Millennials make up a greater share of the workforce. And the challenge is greater for small-to-medium sized businesses (SMBs), who are at a disadvantage compared to their larger counterparts with deeper pockets.

It used to be that a good salary and solid benefits were enough to win an employee’s loyalty for years or even decades. That started changing in 2008 as the job market became less stable and accelerated as the economy recovered and more Millennials entered the workforce. Not only has it become a job seeker market, but what employees are seeking from their jobs has changed. Work and salary are no longer ends in themselves but need to be means to something greater for employees to stick around. Many, particularly younger employees want personal development and meaningful work. As a result, people are staying in their jobs for 2-3 year stints before moving onto the next position that offers them an opportunity for growth and fulfillment. They want workplaces where they feel supported and cared for, otherwise they will leave for somewhere that provides that for them.

And employee benefits are a vital part of any strategy to meet those needs to attract and retain talent. An Aflac survey found that most employees would change jobs for a lower salary but better employment benefits. Unsurprisingly, the same survey found that 80% of respondents believed that their employee benefits plan influences their engagement in their jobs. Competitive benefits are a necessary component for an effective strategy to build and engage your team so that you can grow your company. But how can small businesses who lack their competitors’ resources offer benefits that will make potential hires choose to work for them or stop current employees from jumping ship?

The answer is to develop a careful employee benefits strategy which minimizes costs while maximizing the impact on employees. And to craft and implement an effective strategy, small businesses need a dedicated benefits broker who understands their unique needs and is willing to be deeply involved in their business. Growing companies cannot afford to pay employee benefits broker commissions to major brokers in exchange for out-of-the-box solutions. They need customized solutions and a small-business approach.

So how do you find the insurance broker who will meet your unique needs? Well, let us outline the basic steps to finding a new health insurance broker and what to look for when choosing your new employee benefits partner.

How to Start the Process to Find a New Health Insurance Broker

What an Insurance Broker Is and What They Do

It’s time for a quick definition, in case this is the first time you are shopping around for a new benefits broker. What exactly is the difference between a health insurance broker and an insurance agent? Well, an insurance agent is employed by a specific insurance provider and is the point of contact between the insurance carrier and the plan purchaser. They might be able to offer discounts and assemble a specific group health insurance plan for employers, but they won’t be able to shop around between different providers to deliver the best results.

An insurance broker, on the other hand, is the representative of the employer rather than of the insurance carrier. They are empowered by the employer to negotiate on their behalf with any and all insurance providers. This means that they can get the best rates in the market rather than from a given carrier and can put together a specialized employee benefits package from multiple providers that meets both the employer’s and the employees’ needs. They can also serve as a benefits consultant to help their clients develop effective benefits strategies.

How to Tell if It’s Time to Find a New Insurance Broker

The first step in your journey to find a new employee benefits broker or insurance broker is to decide whether or not you need a new broker. We’ve covered this topic extensively in a previous article but here are some clear warning signs that it’s probably time to start your employee benefits broker search:

• Renewing the same employee benefits package year over year with little consideration for a long-term benefits strategy

• Receiving less guidance or a lower standard of customer service from your insurance broker

• Going several years without reexamining the benefits broker relationship

• Finding it difficult to determine ROI that justifies investment in your current health insurance broker

How to Start the Search for an Insurance Broker

Once you’ve decided to find a new employee benefits broker, you should define your goals for your benefits plan. This will help you find a partner who will work with you to meet those goals. Do you want to reduce costs for your existing healthcare benefits so that you can expand other benefits your employees value like dental or vision insurance? Or do you want to completely restructure your entire employee benefits plan?

Based on these goals, set the criteria to define promising health insurance brokers based on these goals and your knowledge of the market. What does your ideal employee benefits broker look like? What do you not want in your next insurance broker? These criteria will also tell you what questions to ask a new benefits broker.

If you want to be extremely thorough, you can input the criteria you identify into a benefits broker Request For Proposal. Think of the benefits broker RFP as a formalized job description for your next benefits broker. Your benefits broker RFP should include a statement of your benefits and health insurance needs but leave room for brokers to “wow” you with additional services. You can then share your broker RFP with brokers who seem promising during your research so that their representatives can tailor their proposals to your unique needs.

What is more important than the procedure for starting your search is knowing what to look for in a broker. You want to set the right goals for your business, identify accurate needs, and put together criteria which will be genuinely useful in choosing a new health insurance broker.

What to Look for In a New Health Insurance Broker

Size and Customer Service Approach

Generally speaking, you want to work with a boutique broker that specializes in SMBs. This is relevant because large brokers will often prioritize their big accounts over your business. Smaller insurance brokers will treat you as a priority no matter how big your business is because every account is an important account for them. An SMB health insurance broker will be much more willing to offer more customized solutions which are tailored to your specific needs. And they won’t have had a chance to develop the bureaucracy which makes working with the largest benefits brokers so frustrating

In addition to overall size, another thing to look for is the benefits broker’s approach to customer service. You should work with an insurance broker who will provide you with a dedicated account manager, access to key players in their organization, and continued support after setting up the initial insurance plan.

Minimizing Expenses While Maximizing Value for Employees

Your new health insurance broker should do everything in their power to minimize your expenses while maximizing value for your employees. Far too many insurance brokers focus on the former and neglect the latter, but both are vital for a successful benefits strategy.

The best employee benefits brokers are proactive in their approach to insurance challenges. First, they identify demonstrated employee needs by conducting health-risk assessments (or HRAs) and other employee surveys to find out what benefits your employees really need. Then they create an employee insurance package which meets those needs while cutting costs from lower priority benefits. These steps are absolutely necessary to effectively minimize costs and maximize impact.

What should the resulting insurance package look like? An effective health insurance broker will put together a flexible and creative company benefits plan. Often, the package will include a tiered insurance structure which allows low-risk employees to choose cheaper plans and other employees to take on more expensive plans in exchange for more comprehensive coverage.

The foundation of the tiered approach for small businesses will be high-deductible health plans (HDHP) paired with health savings accounts. These plans allow employees to take on more responsibility for and control over their healthcare expenses. They provide a much higher standard of care than the ‘catastrophe insurance’ which is becoming popular but at a low cost to both employer and employee. And thanks to a brand new IRS rule, HDHPs can now offer more preventive care at low-deductibles to reduce your business’ healthcare expenses in the long-term.

Ask potential insurance brokers what they can do for your business. If they answer in terms of both what they will do to help your bottom line and what their plans will do to help your employees stay happy and healthy, odds are that they will be a great partner for your growing business. If not, they’re almost certainly not the right choice for you.

Creative Employee Benefits: Wellness Benefits and More

A great health insurance broker won’t stop at the conventional. They will be at the forefront of the benefits conversation, offering uncommon benefits which will help you stand out in the competitive employer marketplace. And one of the biggest areas which your new employee benefits broker should cover is wellness benefits. These benefits include smoking-cessation and weight-loss programs, gym memberships and nutritional programs, and other ‘lifestyle’ benefits.

Your insurance broker should not just want to put out fires after they’ve started, but rather should head off expenses at the pass. Wellness benefits can prevent healthcare expenses from lifestyle-related illnesses, which represent a full 70% of all healthcare costs. That’s one reason why wellness benefits have an average ROI of 3:1. Plus, they do a great job of making employees feel valued, taken care of, and engaged in their work at the same time as they are saving your money.

Employee Benefits Technology

Another important factor to consider when choosing an employee benefits broker is what employee benefits technology they offer. Generally, brokers will offer two different kinds of technology: benefits enrollment technology and telemedicine.

Benefits enrollment technology is software which can be used to facilitate the benefits experience for your HR team and your employees. The best employee benefits brokers will offer top-of-the-line enrollment software to streamline open enrollment and record the necessary compliance information. They may also offer a company benefits portal which allows employees to review and manage their benefits, request time off, and learn about their healthcare options.

On another note, telemedicine is transforming the way that employees access healthcare. Allowing employees to consult doctors digitally keeps them healthier, reduces costs for everyone involved, and reduces absenteeism. Other software solutions can offer pharmacy discounts, notify employees of nearby providers, and otherwise streamline the healthcare experience for your employees.

How to Tell that a Boutique Health Insurance Broker Can Deliver the Goods

Proven Track Record of Success

Actions and results speak much louder than words and results are the best way to measure the worthiness of a potential health insurance broker. A benefits broker worth their salt will be able to provide you with evidence of past success with clients who are like you. You should look at their website to see if they have published any client case studies. If they do, that’s a great sign in-and-of-itself because it shows that their clients are happy with their results. But you should also take the time to read through the case studies to see if the insurance broker provided their client with the kind of services that you are looking for at your business.

The greatest test of a broker, though, is whether they will let you talk to any current clients to get a truly unfiltered perspective on what working with them will look like. Giving access to their clients is a real sign of trustworthiness and a testament to the kind of relationship that a broker has with their clients. As an employer, you ask for a list of references from any potential hires. You created a job listing with your benefits broker RFP, why shouldn’t you ask for references as well?

Key Takeaways for Finding an Insurance Broker

The decision of how to choose a new health insurance broker is a pretty big deal. The right broker can help you cut costs, provide more value for your employees, and win the war for talent by attracting, retaining, and engaging the talent your business needs to succeed. This can sometimes seem like an overwhelming task. Hopefully, this article has given you a good idea to start. Just remember: • Decide what you want to accomplish with your health insurance plan and employee benefits package so that you know what to look for in an insurance broker • Put together a benefits broker RFP to help define what you’re looking for and solicit proposals • Boutique brokers will make growing businesses a top-priority and provide more customized, hands-on service • Questions to ask a new benefits broker include whether they provide wellness benefits, tiered benefits, and benefits technology • Pick a broker who takes an approach that both minimizes expenses and maximizes impact for employees; focusing on just one isn’t enough • Brokers with a proven track record of success and provide case studies or even direct access to clients are a much safer bet than unknowns

Are you interested in working with a more proactive broker who helps you maximize the human potential of your business? Learn more about Launchways today.

Amid legislation that pushes consumerism in healthcare while putting greater burdens on healthcare consumers, employers and employees alike have turned to high-deductible health plans (HDHPs) to minimize their healthcare costs. As premiums continue to rise, these plans offer an opportunity to keep upfront costs low for companies and their employees. At the same time, the IRS permits the creation of tax-exempt health savings accounts or HSAs for people with HDHPs to cover the costs of the higher deductibles when expenses do come up.

This system works great for everyone involved – so long as people stay healthy. Which makes preventive care an integral part of any successful HDHP based healthcare strategy. By allowing patients to head off health issues before they become significant expenses, preventive care keeps everyone’s expenses down and maximizes health outcomes for the insured. Recognizing this, the IRS has allowed insurance plans to cover preventive care such as check-ups, screenings, immunizations, and tobacco cessation or weight-loss programs with a low or non-existent deductible while keeping their HDHP status.

However, the IRS has not generally extended the same low-deductible permissions to treatments for existing illnesses or conditions. Since 2004, certain on-the-spot treatments for conditions discovered during screenings (such as removing polyps discovered during colonoscopies) and medications to prevent recurrence of heart attacks or to reduce cholesterol to prevent heart disease have fallen under the umbrella of preventive care, but that’s about it.

Which means that people with chronic conditions have generally been left out. They have had to choose between paying out high-deductibles for treatments that prevent their conditions from worsening, or giving up their HSAs and adopting high-premium plans. Until now, that is.

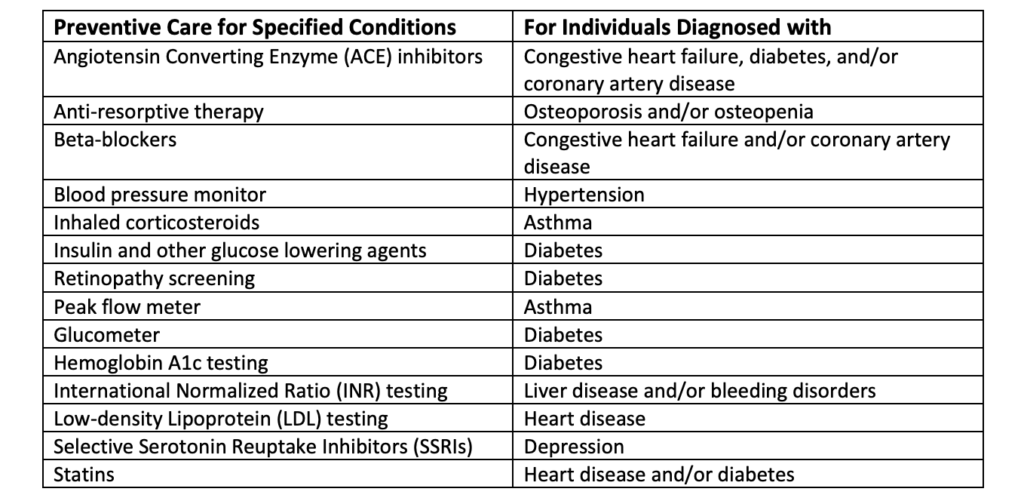

The IRS’ New Rule

On July 17, 2019, the IRS issued Notice 2019-45, which significantly broadened the definition of preventive care to extend it to many treatments for chronic conditions. To qualify as preventive care, the treatments must be likely to prevent the worsening of a chronic condition or the development of a secondary condition which would incur greater healthcare costs. It must also meet several other criteria, which we have outlined in this handy chart for easy reference:

The Impact for Companies and Their Employees

So what does this policy change mean for employers and employees? Simply put, it provides enormous opportunities for both to take greater control over their costs, minimizing their expenses while maximizing employee health and wellness. It makes the already appealing HDHP and HSA healthcare option a win for employees who want to increase their welfare and for employers who are looking to reduce their expenses.

The expanded definition of preventive care provides a new opportunity for employers to educate their employees so that they can become more intelligent consumers amid government policies which force consumerism in the healthcare market. Employees can use HDHPs to control their costs without fear of compromising their health, especially by neglecting chronic conditions to avoid paying high deductibles. Instead, they can get the treatment that they need at low costs while keeping their tax-exempt health savings.

Key Takeaways

We’ve thrown a lot of information your way in this article, so here are some key takeaways that you should remember:

• IRS Notice 2019-45 opened up serious opportunities for employers to cut their costs and for employees to reduce their expenses and maximize their healthcare outcomes

• Chronic conditions will no longer force consumers to take on significant healthcare costs to receive the treatment they need to maintain their health and avoid future expenses

• That means that high-deductible health plans, which already provided the best solution for consumers in the current healthcare market, are now better than ever

To make the most of the rule change as an employer, you should partner with a proactive benefits broker who will help you craft a healthcare strategy which maximizes the impact for your employees while minimizing your costs. Benefits are an important tool to attract, retain, and engage the talent that you need to grow your business. The well-being of your company and its employees ultimately depends on the effectiveness of your benefits strategy. So it is more important than ever to work with the right benefits broker.

Interested in making the switch to a broker who is invested in your growth and your employees’ well-being? Start the conversation today.

When was the last time you considered how well your employee benefits broker was performing? In the intense war for talent that we’re now experiencing across industries, you can’t risk overlooking any aspect of recruitment and retention strategy.

Employee benefits are one of your most effective tools to attract top talent and retain the top performers you have. With more open jobs that unemployed people currently in the US, recruiters and executives must do everything possible to keep their organization competitive in the talent marketplace.

The employee benefits broker your business works with plays a large role in how impactful your overall benefits offering in your ability to attract and retain talent. Think through the crucial questions outlined in this post will help you ensure that you’re working with a benefits broker that’s doing the most for your business.

1.Conduct a straightforward costs and benefits analysis

First of all, the amount of money you put into your employee benefits program is no small expense for your company. For most companies, benefits are the second most costly expense, just behind salaries, according to data from the Society for Human Resource Management (SHRM). So, it’s a smart decision to enlist a skilled benefits broker to ensure those costs are kept low while driving the maximum value for your business. But you must consider how much value is your current broker providing to your business? And what are the measurable advantages that you can directly correlate back to their services?

The truth is, your broker may be providing subpar services that aren’t getting you the results you want or need (or that are visible to employees). What you need to happen: the money you put into a benefits program is well spent, and you don’t have to continuously worry about what your funds are going toward. You have too much on your plate to have to then keep tabs on your benefits broker, so review your current benefits program and employee satisfaction level to determine if your broker is meeting the mark.

2. Consider the latest technologies: Is your broker keeping up?

Approaches to employee benefits administration continue to be updated based on what’s happening in technology and business intelligence. When was the last time you had a conversation with your benefits broker about how they’re using these advances to push forward your company’s benefits strategy? If this conversation has never been had, or if you feel like your benefits broker isn’t using some of these technologies the way they could, it may be time to find a new employee benefits consultant.

Part of your role in choosing a benefits broker is ensuring that you find someone who not only recognizes the importance of proactive change, but who also incorporates these updates into the way they do business. It should be their responsibility to know what’s hot in the benefits market and what high-quality candidates are looking for, so that they can make effective recommendations to you and your team about offerings and updates. If your employee benefits broker is behind the times, your benefits package will be, too. And if that’s the case, you’ll have a much more difficult time attracting and retaining the best talent.

3. Assess business growth (or lack thereof)

If your organization is growing, chances are you need to make updates to many of the vendors or consultants you work with. Benefits brokers are no exception, as these professionals typically have specialties in regards to the size, industry, and culture of the companies they work with. If your workforce is growing rapidly, it may be time to assess whether a different broker would bring you better results.

When your company changes, it’s always a good idea to take a look at if your benefits broker can still provide the level of services you need. It may be especially smart to look at current and historical growth information and projections around the time when it’s time to think about revamping your employee benefits package for the coming year.

4. You haven’t looked around in a while

It’s of course easy to let consultant-shopping fall by the wayside once you’ve hired someone and have gotten used to working together. But when was the last time you looked around to see what else is out there? Even if you don’t end up hiring a new benefits broker, just taking this step could mean that you will reaffirm your decision in hiring your current broker. You may already have the best, most cost-effective person for the job—but you’ll never know if you don’t keep up with your research. If it’s been more than three years, as the SHRM suggests, start shopping for a new broker now, even if you don’t take any further steps forward beyond exploring your options.

5. Service and communication have been lacking

We’ve all experienced when a vendor just isn’t performing up to par. It can be easy to make excuses for these professionals or to hand out too many second chances, especially if we like the person and really want the business relationship to work out. But, we often end up having to do more work than we should be doing in these instances.

Remember: you’ve hired a benefits broker for a specific job. Really think about if they are providing every required aspect of that job, and ideally going above and beyond what is expected to provide the highest level of service. If you’re having to correct their mistakes, call or email them more than once for a response, or remind them about deadlines or new strategies to try, it’s probably time to call it quits and find a broker who will step up and provide everything you need.

6. Employees aren’t satisfied with the benefits program or with the enrollment process

In today’s candidate-driven job market, employees are often on the lookout for a better position. Even if they’re satisfied with their work, their role, and their company, they are always keeping their eyes open to make sure there isn’t something even better out there. One survey conducted showed that 78% of people are open to new jobs in 2019, and 38% reported to be actively searching for a new role.

Benefits play a large role in employees’ decisions about whether to stay or leave. So how happy are your workers with their current benefits package? You may hear complaints or praise at lunch or in the hall, and that could be helpful information when you’re starting to think about your benefits broker. Or, you may even want to implement a benefits survey where employees will feel encouraged to share what they don’t like or what they’d like added in the near future.

This can be a great way to find out if your benefits broker is getting you the package that includes everything the modern employee wants, from plenty of parental leave to gym memberships to excellent health and dental packages, and more.

But, there’s more to benefits satisfaction than just the benefits themselves—employees also care about the benefits portal and having easy access to benefits information. Assess whether information is readily and easily available to all employees.

What kind of benefits technology does your current broker use? The enrollment process should also be streamlined and simple so that employees aren’t dealing with a big headache once a year to get the benefits they want and need. You need a broker consultant who will use the latest tools to ensure that processes are simple and transparent for your employees.

Key takeaways

The person behind your employee benefits package and process has a lot of influence on employee satisfaction and your ability to attract high-quality candidates. When you’re assessing whether it’s time to find a new benefits broker, consider:

If the costs versus benefits are aligned

If your broker is keeping up with the latest trends and technologies

If your organization has grown significantly and may have new needs that your current broker can’t provide

If it’s been more than three years since you shopped around

If your broker’s communication and services haven’t been up to par

If employees are complaining or aren’t satisfied with their current benefits package

If some of these considerations are true for you and your organization, it may be time to start shopping around for a new employee benefits broker. Remember that before you make a selection, it’s important to list all the ways your previous broker was not meeting expectations so that you don’t make the same mistakes again.

One of the main reasons why many companies stay with the same benefits broker year after year is because they have a personal relationship with them. Maybe they’re brothers-in-law, golf buddies, or business school friends. There’s a good reason for that – connections are important for business success, they might feel more comfortable being upfront with a broker they know, and sticking with the same broker can give a sense of stability often lacking in a growing business. But at the same time, these relationships often cause businesses to stay with the same broker even after they have stopped providing the highest level of service.

No matter how great, personal, and long-lasting your connection is with your current broker, it is always a good idea to reevaluate the relationship. This does not mean just ditching your current broker because there might be someone else out there who will do more for your business. It simply means taking an honest look at your current broker to see if they are still doing everything possible to help your company grow and succeed. And then, if you have doubts, looking at what competitors are offering to see if you could benefit your business by switching brokers.

If that idea makes you uneasy, we get it. Honestly evaluating your business relationships and potentially changing them can be difficult and sometimes painful. It’s much easier to just let things stay the way they are. But if you do, you will be doing yourself, your business, and most importantly, your employees, a huge disservice. So we’ve broken down the steps that you can take to make sure that your current broker is still the best fit for your business, no matter what relationship you have with them. In this article we’ll explore:

• Why You Should Care About Your Broker

• Risks and Rewards of Working with the Same Broker

• How to Evaluate Your Broker

• What to Do When Your Broker is Friends with Your CEO

Why You Should Care About Your Broker

Many growth-stage businesses treat benefits as a necessary evil and as such, they choose the path of least resistance. This may mean working with their buddy, or it could mean working with a broker who doesn’t push them think about their long-term benefits strategy, even if that means that their employees end up with subpar benefits at a higher cost. But the fact of the matter is that employee benefits are a crucial component to the success or failure of a growing business.

Benefits spend is generally the single largest talent-related cost after base salary. That means that minimizing benefits expenses is extremely important to the financial sustainability of growing businesses, especially given the small margins most operate upon. You want to work with a broker who does absolutely everything that they can to reduce your benefits spend while maintaining or increasing the quality of benefits for employees.

And benefits don’t just matter to your bottom line. They are one of the biggest tools in your arsenal to attract, retain, and motivate top talent. According to Aflac surveys, most employees would accept a job with lower compensation but a better benefits package. And the same survey found that 80% of employees believe that their benefits package influences their engagement in their jobs. Building an effective, motivated team of talented employees is vital to the success of any business. But many struggle to compete for talent against large companies with greater resources. A targeted, intelligent benefits strategy which maximizes impact while minimizing costs can help growing businesses attract the talent that they need.

To have this impact on your employees and your finances, though, you need to work with a benefits broker who understands your unique needs and who is constantly working to update and optimize your benefits package. It’s not enough to set up your benefits package and then forget about it or to work with the same broker year after year without considering whether they’re delivering the maximum value for your business (even if they are your brother-in-law).

Risks and Rewards of Working with the Same Broker

Are there plus sides of working with the same broker, especially if you have a close relationship with them? Of course there are. They might advocate harder for your business because of their relationship with you, provide more personalized service, and serve as a more effective sounding board for your benefits strategies. Plus, it’s nice to do business with someone who you know and like.

At the same time, though, those same feelings that give you pause about the idea of changing brokers can also hold you back from being a fierce advocate for your business and its employees. You might be afraid of damaging your relationship by pushing your broker to provide the most effective, and affordable, benefits package possible. Failing to keep business relationships and personal relationships separate can often lead to sub-optimal business results or even conflict and damage to both relationships.

And it’s not just your attitude that matters. Most brokers, no matter how good their intentions are, will start taking accounts that they feel are ‘safe’ for granted. They’ll focus their time and resources on pleasing their new clients and acquiring new accounts. And no account is safer than one that is secured by friendship or family connection. Your brother-in-law or college buddy might well work extra hard to get you a good deal when setting up your benefits package. But chances are that they’ll start taking your business for granted, especially as the years pass by. The level of service will decrease, your benefits package will get outdated, and you will lose your competitive edge to attract and retain the talent you need to succeed.

How to Evaluate Your Broker

There’s no harm in finding out whether or not your current broker is providing the maximum value to your business. Taking an honest look at your benefits strategy and your benefits broker only helps you improve your employees’ lives and your business’ finances no matter what you decide to do with the information.

So how do you tell whether your broker is still the best fit for your business? Here are some key things to ask yourself when evaluating your broker:

• Have they updated your benefits package recently? If your benefits haven’t changed in a long time, it’s likely your current broker isn’t taking a critical look at how to constantly improve your offering.

• Are they working with you to refine your benefits strategy based on your business needs and the needs of your employees?

• Can you demonstrate ROI to justify your investment in your broker?

• Is your broker working with you to develop innovative solutions to maximize value and minimize costs?

• Does your broker identify and address your employees’ real needs? Brokers can conduct employee surveys and health-risk assessments (HRAs) to identify employee needs and adapt your benefits strategy to meet them.

• Is your broker leveraging the latest in benefits technology? Telemedicine, enrollment software, and a centralized benefits administration platform are all tools that can make a big difference for growing businesses.

• Do your employees report a high level of satisfaction with their benefits?

• Have your benefits expenses per employee been going down year over year? If not, your broker might not be doing everything they can to minimize your costs.

If you find that many of these questions can be answered with a ‘no’ and your broker is unwilling to adapt to meet these challenges, then it may be time to do some serious thinking. It isn’t worth staying with a broker who is underperforming and damaging your business, no matter how great your relationship with them is.

What to Do if Your Broker is Friends with Your CEO

One of the worst positions you can find yourself in as an HR or Finance professional is being dissatisfied with a broker who is buddies with your CEO or a board member. You understand what’s best for the business, but your hands are tied by your higher-ups’ relationship with the ineffective broker. How can you go about convincing them that it is time to reevaluate the relationship?

Of course, you can always send them this article. But that in itself may not be sufficient. The first thing you should do is collect as much information as you can. Research the latest benefits and technology, what other brokers offer, and what other companies pay for their benefits. Conduct employee surveys to identify employee needs and attitudes towards the current benefits. It might even be a good idea to solicit quotes from other brokers so that you can provide concrete alternatives when presenting your position to your CEO or board.

The next step is to use this information to craft a business case for switching or reevaluating brokers. Focus on ROI in terms of benefits expense savings and talent acquisition, retention, and engagement. Whenever possible, back your claims up with data. Draw a comprehensive picture of your company’s current benefits package and its performance, and then use your research to show how it can be improved.

If you draft an effective business case you will hopefully convince your higher-ups that something should be done about the company’s benefits. It’s now up to you to show them the path forward. Outline the steps involved in switching brokers (did you know that switching brokers is extremely simple?). If you’ve already gotten initial quotes, you can use these to smooth the transition to a more proactive broker. Not only will explaining the next steps help you make your case, but it also will help ensure that action is taken to remedy the situation. Companies often hesitate to take these kinds of big steps out of fear that they will disrupt the business’s operations. Laying out a clear path forward, along with its costs, savings, and effect on employee experience can make the difference between staying with your current broker and taking the next step to help your business grow and succeed.

Key Takeaways

We’ve covered a lot of ground in this article and reevaluating your relationship with your benefits broker is a highly complicated and charged topic, so we don’t expect you to have it all down right away. Feel free to refer back to this article whenever you need a refresher, and keep in mind the key points we’ve covered:

• Your employee benefits are your second biggest talent-related expense and one of your primary tools to attract, retain, and engage the talent your business needs to grow and succeed. So taking a strategic approach to working with your broker is incredibly important to your business’s health. Even if it means reevaluating your business relationship with a broker who is also your friend or family member.

• Unfortunately, brokers who you have a personal relationship with will often take your business for granted. That means that they will start providing a lower level of service, fail to update your benefits, and not work as hard to minimize your costs while maximizing value for your business.

• It’s a good idea to make an objective evaluation of your current broker so that you can get them to deliver better results for your company and its employees or so that you can find a more proactive broker.

• If you’re ready to change brokers but your higher-up has a relationship with the existing broker, then you need to craft a business case for switching brokers using as much data as you can collect, and you should outline the steps necessary to change brokers.

Your benefits broker has too much power over your business’s long-term success for you to rely on the same broker based on a sense of obligation due to your existing relationship. Reevaluating that relationship will allow you to maximize the value for your business and its employees, whether you change brokers or not.

Many companies stay with the same employee benefits broker just because they are afraid that switching will be too difficult. They imagine that changing benefits brokers will entail a lot of paperwork, direct communication with insurance carriers, and major changes to their insurance plans and benefits package. The disruption caused by such a shift would certainly outweigh the advantages of switching to a new broker, at least in the short-term. So they stick with the broker they know rather than working with a broker that will best meet their needs long-term.

But the fact of the matter is that it really isn’t that hard to change benefits brokers. It doesn’t take a lot of time and doesn’t require major changes in your benefits package or internal processes. So there is no reason to stay with a broker you’re dissatisfied with because you are afraid of what changing might involve. In this article we’ll address some of the misconceptions that you might have about switching brokers and outline how easy and rewarding the process really can be. The key points which we will cover in this article are:

• You can keep your insurance carriers and plans

• You can switch any time throughout the year or phase of the renewal process

• If you want to change insurance plans or carriers, the process is quite easy with the right benefits broker

• Switching benefits brokers can produce serious results for your business

You Don’t Have to Switch Insurance Carriers or Change Benefits Packages

Despite what many people think, changing employee benefits brokers does not mean that you need to change your benefits package or insurance carriers. You simply need to notify your insurance carriers that the new benefits broker is representing you instead of the old broker. You do this by submitting a Broker of Record (BOR) form to the carriers, which enables the new broker to negotiate with the carriers on your behalf, monitor rates, and advise you on the best benefits package. To make things even easier, your benefits broker can handle the process of drafting and sending the BOR, you just need to sign it.

Now, you may wonder why you would switch employee benefits brokers if you’re just going to keep the same insurance plans. But your healthcare plan is only one part of the overall benefits picture. A good benefits broker will be able to work with you to optimize your benefits package or phase in a new one without disrupting your employees’ experience or internal processes. Plus, a great benefits broker can streamline and improve the benefits experience for you and your employees within the same plan structure. They can provide increased service and support, including employee education initiatives and enrollment or benefits administration software platforms. And they can also negotiate new, lower rates for the same plans at the next renewal.

There Are No Time Constraints on Switching Benefits Brokers

You don’t have to make the switch to a new employee benefits broker at a particular time of year or phase of the renewal process. You can submit the BOR at any time and since doing so won’t require that you change your benefits package, the timing for when to change benefits brokers doesn’t depend on whether or not you’re ready to change your benefits package. Your internal processes will not have to change, and your employees won’t notice any difference in their benefits experience.

This means that you can switch benefits brokers as soon as you have found the right partner for your business. That way the new broker will have access to the information they need to start advising you on your benefits strategy and optimizing your benefits package. You can work together to craft a better approach to benefits and phase in your new benefits initiatives while providing a seamless experience for your employees.

With the Right Benefits Broker Switching Insurance Plans Isn’t Difficult

While you do not have to change your benefits package when you switch benefits brokers, you can explore options for an improved benefits package to your employees at a lower cost to the company. This may sound daunting, but it’s really not very difficult or even that time consuming when you partner with a strategic-thinking, proactive benefits broker.

Don’t get us wrong, switching plans does require a slightly longer transition period, but it’s still not that complicated relative to renewing your existing plans. Plus, most of the work will be handled by your benefits broker.

The first thing that your new benefits broker will do is take a census of your employees to collect the information that they need to assemble your new benefits package. Then they will send out an RFP and collect proposals from different carriers to provide you with the best possible options to choose from. Or, if you have established carrier relationships and preferred plans, they will get an updated quote based on your specific needs and your employee data.

Once you and your broker select a carrier, it’s time to enroll your employees in their new insurance plans. Now, the words “open enrollment” might send most HR professionals running for the hills, but a good broker will actually make this process painless. Many benefits brokers will provide centralized platforms for employees to view and enroll in plans and for your HR team to store data to monitor compliance. And boutique benefits brokers will work directly with your employees to educate them about their new insurance options and the enrollment process in general.

At the end of the day, if you’ve picked a great benefits broker, your role in the transition to a new benefits package will be minimal.

Switching Benefits Brokers Can Reap Real Rewards for Your Business

Not only is switching brokers a lot easier than people expect, but it can also be seriously important to your business’ success. According to a Met Life survey, 76% of employers believe that brokers help them get the best possible prices on employee benefits, and nearly as many say that their brokers help them to stay compliant. If you don’t feel like your broker is doing enough to help minimize your costs, maintain compliance, and provide the best possible benefits for your employees, then switching is well worth the minimal inconvenience.

The fact of the matter is that benefits spend is a huge part of your overall budget and makes up 25-40% of most companies’ payroll. So it’s important to work with the right partner to minimize those expenses while maximizing the return-on-investment of the remaining expenses. For instance, a great benefits broker will reduce your benefits costs by strategically designing plans that are the right fit for your employee demographics and helping employees become better consumers of their healthcare. They can also reduce costs by introducing discount prescription drug plans, technological solutions like telemedicine and wellness programs that help prevent long-term expenses from lifestyle diseases.

More importantly, your benefits package is one of the greatest tools in your arsenal to attract, retain, and engage great talent that will help your business grow and succeed. According to an Aflac survey, 80% of employees believe that their benefits package influences their engagement in their jobs. In addition, most said that they were likely to accept a job with lower compensation and better benefits. Clearly, compelling benefits are essential to any effort to attract top talent as well as maximize employee productivity and retention.

Your new broker will be able to provide the best possible package for your employees by conducting third-party surveys to identify their needs and then crafting a benefits strategy to meet those needs. All while reducing costs by eliminating benefits that your employees don’t need or want.

Finally, if you pick the right benefits broker, they will see each of your employees as their clients, rather than just focusing on appeasing your company’s top executives. These benefits brokers will work on the individual employee level through seminars, Q&A sessions, and other forms of direct communication. This hands-on approach will help employees understand how to navigate the benefits package and make the most of the benefits offered. It will also impress upon employees the value of the benefits in order to maximize the impact that your benefits have on employee retention and engagement.

Key Takeaways

Changing employee benefits brokers may seem like a very daunting decision, but the actual process of making the switch once you have found the right benefits broker is surprisingly easy. Plus, with so much on the line when it comes to your employee benefits package, the minimal amount of effort required is well worth it. Because at the end of the day:

• You can keep your insurance carriers when you change your benefits broker

• You can change benefits brokers any time or phase of the benefits renewal process

• Switching insurance carriers is quite easy with the right benefits broker

• Your benefits broker is responsible for managing up to 40% of your payroll costs, so make sure you’re partnering with the right broker for the most cost-savings and best return on your benefits dollars invested

So switching brokers isn’t that difficult, but you do need to find the right partner. Want to make sure your current broker is serving your needs? We wrote a handy article that will show you how to evaluate your existing broker. Check it out right here.