In the year 1970, per capita annual health care costs averaged around $1,848 (in today’s dollars). In 2019, that number increased to $11,582.

Over the last forty years, this increase in health care costs has reached the pockets of employers—on average health care costs are more expensive now than they have ever been before.

This change has led company CFO’s to take a much more active and expended role in health plan design. In this post, we’ll discuss this trend.

Specifically, we’ll talk about:

The Ongoing and Increasing Trend of CFO Involvement in Health Plan Design

What Is Causing This Trend

What Should Business Leaders Do About This

The data covered in this article was collected by cutting-edge benefits firms that collectively support thousands of employers across the U.S.

The Ongoing and Increasing Trend of CFO Involvement in Health Plan Design

A recent survey has produced significant evidence that supports the idea that CFO involvement in health plan design will continue to increase. Consider the following findings from the survey:

Over the past three years, only 32% of organizations have made changes to manage health care costs. However, 55% of organizations expect to make changes over the next three years.

74% of business leaders indicate that their finance department has had an active role in making decisions related to their health care program over the last three years. However, this number increases to 87% when asked if their finance department will have an active role in the health care program over the next three years.

48% of business leaders stated that their finance and HR departments shared responsibility for the organization’s overall health care management and strategy over the last three years. When asked the same question about what they expect over the next three years, the number increased to 58%.

The data is clear. Health care costs are increasing, and organizations will be making changes in the near-term future to adapt. These changes will involve an increased role of the CFO (and the finance department in general) in the management of the organization’s health care program.

What Is Causing This Trend

The driving forces behind the trend explained in the previous section are both simple and complex at the same time.

From a simple perspective, the trend is being caused by a decades-long increase in health care costs for employers. In order for company leadership to manage the rising costs of their health care plan, they must instruct the CFO and the finance department to have an increased role in decisions related to the plan.

However, recent events have made this trend even more complex. The COVID-19 pandemic has created many questions about the future of health care around the globe and the associated costs. Unfortunately, many of these questions remain unanswered. CFOs must become increasingly involved in health care plan management in order to brace for whatever storm lies ahead in the industry.

What Should Business Leaders Do About This Trend?

It may seem as if an increased role of the CFO in what has traditionally been an HR realm will be sure to cause contention within many organizations. The minds of CFOs and HR managers functions differently, there is no doubt about that.

Fortunately, there are many trusted sources of support to help organizations adapt to these structural and responsibility changes.

According to findings from the same survey that was cited earlier, “Nearly all employers think strategic conversations and innovative solutions are valuable in their relationship with a consultant or broker.” In other words, business leaders are becoming increasingly willing to work with benefits consultants and brokers to help them navigate the uncertain future of the health care industry.

The following solutions which are traditionally provided by benefits consultants and brokers were specifically mentioned in the survey:

Innovative solutions

Strategic conversations

Benchmarking

Market developments and industry trends

Actuarial and financial advice

Fully bundled services and solutions

Business leaders who took the survey overwhelmingly indicated that they will find significant value in discussing the above items with benefits consultants or brokers moving forward.

If you and your business find yourself in need of a more hands-on benefits consultant, be sure that you know what to look for when considering different options. Consider the following tips:

Make sure the broker offers services that can be adapted to your specific needs and business model.

Consider the broker’s approach to cost-savings. Will they offer your business cutting-edge plan design options in order to control benefits spend?

Take a close look at the pricing model of the consultant or broker. Do they work on a commission or fee only basis?

Key Takeaways

Health care costs are increasing, both for individuals as well as businesses. A result of this trend is that company CFOs and finance departments are becoming increasingly involved with the management and decisions related to the company’s health care program. As we soon will enter the post-pandemic world, there is much uncertainty related to what effect the lingering effects of COVID-19 will have on the global health care system. Due to this uncertainty, it will become even more important for the CFOs to be involved moving forward. Businesses can adapt to this trend in healthy ways by working with a more hands-on benefits broker.

COVID-19 changed the landscape in just about every aspect of our daily lives, including the way we work, the way we live, and, as employers, the way we provide access to healthcare to our teams.

This year, we expect to see the continued growth of many themes and trends at a pace that before seemed impossible. COVID-19 shook the healthcare industry, disrupting the normal course of innovation in unimaginable ways. However, this set a new precedent – one in which no aspect of our healthcare structure is seen as unchangeable.

Rapid Growth in Telehealth

Last year, mandatory shutdowns due to COVID-19 created considerable demand for telehealth services. However, although the majority of mandatory shutdowns have since been lifted, the utilization of telehealth services remains higher than ever before. Before the pandemic, telehealth visits made up only 1% of total visits. While this number jumped to nearly 50% amidst shutdowns in April of 2020, telehealth visits now make up roughly 11% of total visits.

In the past, telehealth was hampered by skepticism and its impersonal regulatory environment. While it was gaining popularity due to its convenience, the progress was slow. One main issue prohibiting the wide adoption of telehealth services was the fees associated with it. However, the Centers for Medicare & Medicaid Services (CMS) most recent fee schedule made temporary changes to reimbursement permanent, making it more accessible.

Improved accessibility and reduced variability of care allow telehealth to offer better population health outcomes – creating buy-in from both providers and consumers. It’s not a matter of if telehealth is a viable method of healthcare, but how it fits into the current system. What is the appropriate mix of remote and in-person care?

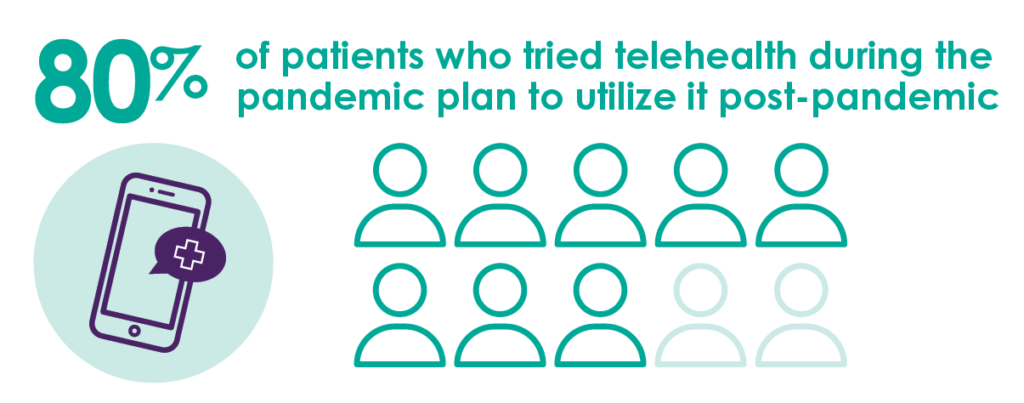

While the new reimbursement structure solidified the concept for many, the popularization of telehealth was gaining momentum with both providers and patients before its implementation. In a recent study conducted by The Harris Poll, research showed that roughly 80% of patients who tried telehealth during the pandemic plan to continue utilizing it.

Aside from primary care – which is poised to be both a long-term and high-volume use for telehealth – other procedures are also vamping up their utilization. For example, mental health services have increased their accessibility through telehealth. This couldn’t come at a better time, given the rising issue of mental health in the U.S. amidst the pandemic. And, telepsychiatric services have become more popular for hospitals and clinics that have limited or no psychiatric staff when treating more severe mental health conditions.

In 2021, if an employee has a phone or computer, they can have access to on-demand healthcare. While more in-depth services might require you to be in-person, the realization that certain parts of the healthcare process can be managed remotely is growing expeditiously.

Technology Driven Healthcare

One place that is often overlooked as a viable clinical setting is an employee’s own home. However, in-home care can be incredibly valuable to many. Those who are able to receive care in-home will benefit from lower costs, and they might even prefer it over the traditional healthcare setting. In turn, many providers are showing an increased interest in an in-home approach to healthcare. This would provide a more holistic list of services including preventative care, ancillary care, and support solutions.

COVID-19 and the impact of the pandemic have permanently shifted the standards of primary healthcare. It has fast-tracked innovation and the embrace of telehealth. With the lack of resistance to this market and the digitization of the entire world, there are several technology-driven trends that you can expect to grow in 2021.

1. Remote Patient Monitoring

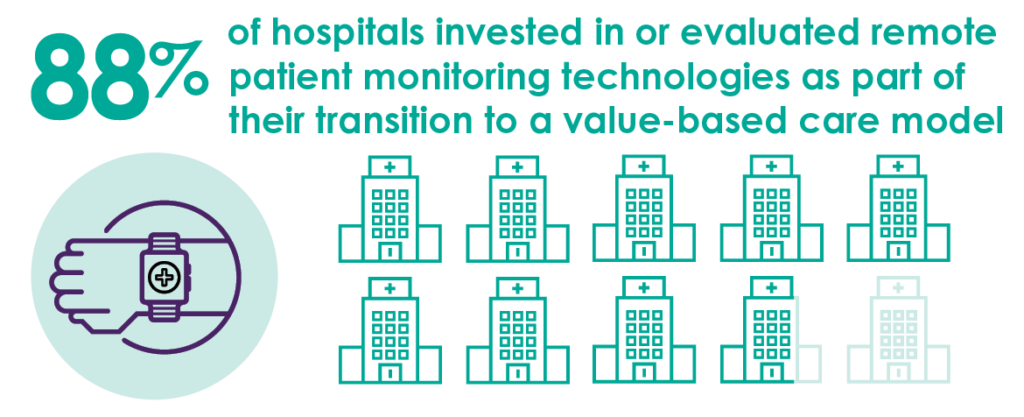

In 2019, roughly 88% of hospitals invested in remote patient monitoring technology. In 2021, remote patient monitoring is expected to continue to grow. As technologies that can monitor vitals become more popular (i.e. smartwatches), monitoring and treating patients suffering from chronic conditions such as diabetes and heart disease.

2. Telehealth

In March of 2020, the CMS began allowing expanded telehealth services through Medicare. As a result, many major insurance providers such as Blue Cross Blue Shield, Humana, and UnitedHealthcare expanded their coverages. At the end of 2020, the CMS completed the permanent expansion of telehealth. In 2021, the utilization of telehealth will continue to grow.

3. Telemedicine

In a recent study by the JAMA Network, research showed that the use of telemedicine in the U.S. increased by nearly 2000% between January and June of 2020. As care delivery to the home continues to grow, providers will also continue to virtually prescribe medications, while relying on remote patient monitoring to help make better care delivery decisions.

Rising Government Populations

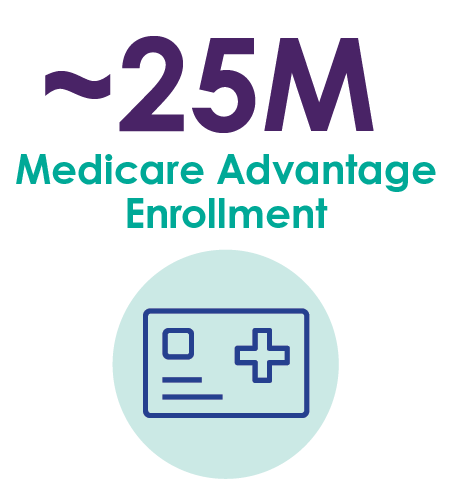

In 2020 we saw rapid growth in the popularity of Medicare Advantage plans. This trend will continue to grow in 2021 as the popularity of managed care and value-based contracting increases. Total enrollment for Medicare Advantage plans in 2020 was nearly 25 million or 40% of all beneficiaries – a 6% increase from the number of enrollments in 2019.

Now that we have a new president and administration in the White House, we can expect to see new priorities with government-sponsored healthcare programs. Possibly the greatest of these shifts in government programs is Medicaid. Between 2017 and 2019, Medicaid enrollment declined consecutively. However, since COVID-19 and its impact on the economy, enrollment is on the rise. In fact, 2020 saw an additional 5 million Americans added to Medicaid.

There is an apparent need for revisions to how we manage and pay the Medicaid population. Low reimbursement rates result in hesitant providers when treating Medicaid patients. This often means extended wait times for Medicaid patients seeking care. It’s no secret, Medicaid patients have long struggled to receive good health outcomes compared to those under commercial healthcare (Medicare), and in some instances, those who are uninsured.

More than 90 million Americans are now covered by Medicaid. That’s up from roughly 75 million before the outbreak of COVID-19. Additionally, the pandemic caused state budgets to tighten, forcing them to look to risk-based contracting arrangements to pay for it. As a result, budgets have become more predictable and the financial risk is moved to the managed care organizations that manage the Medicaid population.

These risk-bearing arrangements bring significant advantages in terms of financial savings due to the co-morbidities and the impact of Medicaid enrollees that have multiple conditions. Better management of these high-cost Medicaid patients could remove considerable amounts from the system. In addition, it increases the possible productivity for the working-age population who need less care.

Self-Funded Employers Will be Empowered to Control Healthcare Costs

While many attempts to curb healthcare costs have been made by providers, employers, and insurers alike, one thing is still apparent – The way that healthcare is both priced and paid for in the U.S. is unsustainable and costs continue to increase across the country. In 2020, both single and family premiums increased by 4% while wages increased by only 3.4% and inflation saw an increase of 2%.

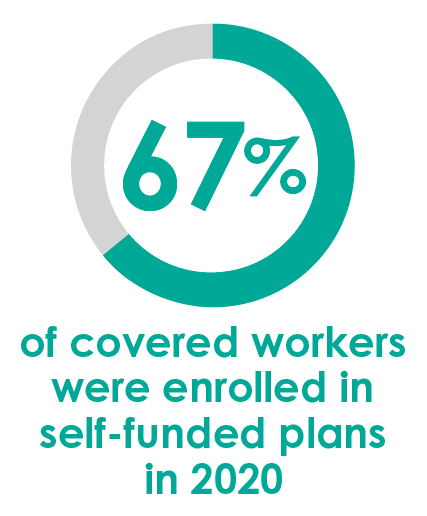

That said, one group has the power to improve the affordability of healthcare for both companies and their employees; self-funded employers. In 2020, 67% of workers with health coverage were enrolled in self-funded healthcare plans. That’s a 6% increase from 2019. Additionally, there were roughly 25 key mergers and acquisition transactions in 2020 in the healthcare space – a 92% increase over 2019. They included reference-based pricing companies, population health applications, care navigation, pharmacy benefits management, and more healthcare plan services. In 2021, we expect to see more growth in these and similar trends.

1. Physician Quality

Avoiding network friction creates limitations to health plans and their ability to guide individuals to physicians based on quality. In response, employers are now searching for ways to navigate members through the use of independent vendors. In 2021, the expectation is that these vendors will continue to utilize quality metrics such as second opinion solutions, physician quality scoring, and centers of excellence to improve their solutions.

2. Pharmacy Cost Containment

The rapid growth of pharmaceutical drug costs continues to be a significant component of healthcare spending, particularly in employer-sponsored health plans. In addition, mid-size and smaller employment groups are receiving poor member and utilization management services from large pharmacy benefits managers. In response, employers are doing more to define pharmacy benefits and participating in aggregation models to create both purchasing power and more focused clinical services.

3. Specialty Condition Management

There has been an increase in popularity for niche solutions, solutions that are built around small yet high-cost employee populations that account for a portion of total healthcare spending. With advanced tech foundations and data analytics, specialty condition management platforms create individualized solutions for employees while offering ROI tracking to employers so they can differentiate from more traditional solutions.

4. Benefit Utilization and Navigation

Better healthcare benefits aside, there is substantial demand for better access, education, and comprehension of the resources that employees have at their disposal. From the physician quality navigation listed above to ecommerce for products and services under the health plans, employers are finding ways to create engagement of the benefits while also managing costs effectively.

Behavioral Healthcare Demand Will Continue to Rise

In 2020, as the stigmas around mental health decreased, the behavioral healthcare market gained momentum. During the pandemic, the demand for behavioral healthcare services saw unprecedented highs as substance abuse, alcoholism, and suicide rates increased across the board. In 2021, we expect the demand for these services will remain strong.

According to a study by Acumen in 2019, research showed that the annual behavioral health market is projected to surpass $240 billion by 2026. Considering that roughly 80% of Americans reported having experienced significant stress due to COVID-19, we expect to see continued growth in individuals seeking behavioral care. In addition, there is a shortage of behavioral health providers in the U.S., and the shortage is expected to grow significantly over the next decade. With this in mind, we expect to see certain trends continue in 2021.

1. Improved Access to Healthcare

With the growing focus on behavioral health, we expect sustained efforts from both the government and private sectors to improve awareness and access to care. With the increased utilization of telehealth and telemedicine services, access to behavioral healthcare is increasing, allowing us to meet the growing mental health crisis in America.

2. Demand for New Solutions

There has been a considerable amount of capital invested into digital health platforms for providers, employers payers, and direct-to-consumer. Expansion of specific segments of behavioral health services is creating a heightened demand for IT solutions with behavioral health technologies. In 2021, we are expecting even more interest in this space from strategic and financial buyers alike.

3. Private Equity Investment

Since 2018, roughly 60 new behavioral health private equity platforms have formed. In 2021, the expectation is that private equity investors will continue to play an increasingly large role in behavioral healthcare.

Millennials make up a significant portion of today’s workforce. Understanding millennial personalities, lifestyles, and well-being is key for many employers to successfully continue the operations of their organizations, especially in the wake of the COVID-19 pandemic.

A recent report published by the Blue Cross Blue Shield Association highlights several concerning health trends among millennials that employers will want to be acutely aware of. The issues associated with these trends could be exacerbated by the COVID-19 pandemic, which adds to the importance of understanding and preparing for the bumpy road of millennial health that lies ahead.

In this post, we’ll provide an overview of two of these key trends:

Rates of behavior health conditions among millennials are increasing.

Millennials with behavioral health conditions are more likely to have a chronic physical condition.

We’ll also briefly talk about what actions employers can take to address these trends in their workforce.

Rates of Behavior Health Conditions Among Millennials Are Increasing

Unfortunately, behavioral health conditions have been rising among millennials. The list below highlights some of the most pertinent conditions and their corresponding increases over the past five years:

ADHD – 39% increase

Tobacco Use Disorder – 10 % increase

Major Depression – 43% increase

Substance Use Disorder – 17% increase

Alcohol Use Disorder – 5% increase

Psychotic Disorders – 26% increase

This data was gathered before the COVID-19 pandemic. As you can imagine, rates of many of these behavioral health conditions are likely to increase even more due to this pandemic. In the report, 92% of millennials said that COVID-19 has had a negative impact on their mental health overall.

Also noted within the research are more statistics that show the frightening effects the pandemic has already had on millennials, “Because of the pandemic, almost 60% of millennials have canceled a health-related appointment or procedure. In addition, isolation, stress and economic insecurity attributed to the pandemic have had a major impact on millennials. Almost 10% have lost their job due to the pandemic, 25% have seen a reduction in their work hours, and 23% have had to access savings to pay for their day to day needs.”

Millennials With Behavioral Health Conditions Are More Likely to Have a Chronic Physical Condition

An extension of the issue described in the previous section is that millennials with behavioral health conditions are more likely to have a chronic physical condition. Specifically, millennials with behavioral health conditions are:

1.9 times more likely to experience hypertension

1.7 times more likely to develop high cholesterol

1.9 times more likely to have Crohn’s Disease/Ulcerative Colitis

2.1 times more likely to have Type II Diabetes

2.7 times more likely to have Coronary Artery Disease

Given that nearly one-third of millennials have behavioral health conditions (and rising), employers should anticipate an increased need to address the above physical conditions in the future.

Millennials seem to be aware of these trends as well. When surveyed, 54% of millennials perceive their mental health as good or excellent, compared to 64% of baby boomers. Further, 80% of millennials believe their mental health has an impact on their physical health, compared to 62% of baby boomers. This shows that many millennials are aware of the mental health issues facing their generation as well as the potential physical health issues that follow.

What Can Employers Do?

Many employers will feel discouraged after reading this post. Millennials will face behavioral and physical health challenges in the future, and employers like you want to do your best to help them.

One of the best strategies that is recommended by Launchways is to work with a trusted and experienced benefits broker. Consider the following ways a benefits broker can help you address the trends discussed in this article:

Guide you as you negotiate with your health service providers to make sure adequate mental and behavioral health services are available for your employees.

Perform an audit of the demographics of your workforce to determine more specifically how it will be affected by these millennial health trends.

Implement strategies to incentivize employees to not skip their routine preventative medical services.

Key Takeaways

The topic of this article is very concerning, especially for employers with workforces that are Millennial-dominant.

Key takeaways from this article include:

Rates of behavioral health conditions have been rising over the last five years.

Individuals with behavioral health conditions are much more likely to experience chronic physical conditions.

The COVID-19 pandemic has already had negative effects on the health of Millennials, and unfortunately there will almost certainly be more negative effects moving forward.

Employers should consider working with a trusted benefits broker, like Launchways, to implement strategies to care for the mental and physical health of their Millennial employees.

Many HR professionals are awaiting key information from insurers on healthcare costs for 2021. Given all the uncertainty surrounding the COVID-19 pandemic and how it will impact healthcare costs for 2021 and beyond, employers may be faced with difficult decisions very soon.

To help employers navigate these uncertain waters, we’ve put together some key considerations that you may useful in light of COVID-19’s impact on the U.S. healthcare system.

In this post, we’ll cover:

Avoiding the traps associated with short term gains

Understanding key industry trends to keep in mind

How to effectively communicate plan decisions to your team

Short-Term Gains are Deceiving

Even with the costs of treating COVID-19, many employers have seen savings in their health plans during 2020. These short-term gains are most likely because many employees have been putting off preventative or elective care due to lockdowns, financial uncertainty, or simply a desire to stay home during the spread of the virus.

Although these decisions have decreased health care costs as a whole during 2020, this trend is unlikely to continue into 2021. Employees will soon return to preventative care regimens, and likely with a much higher demand that usual, and a winter season during the pandemic could lead to an increase in costs to treat COVID-19. These two factors combined could lead to a substantial increase in healthcare costs, and employers should plan accordingly.

Nearly 32% of companies are considering, “Adding, expanding or incentivizing virtual care, telemedicine, and/or remote/online digital care.” On a related note, 66% of companies anticipate virtual health and wellbeing offerings becoming permanent fixtures in the workplace.

Nearly 20% of companies are likely to change health care plans, or at least change the design of the health care plan, to share more costs with employees.

Over 55% of companies are currently conducting, or are planning to conduct, on-site temperature screenings, and 40% are considering on-site symptom questionnaires. Both of these trends are presumably to help employers catch potential infections early on and reduce workplace spread.

16% of companies are planning to add or expand voluntary benefits. Doing so can help fill the gaps with things like hospital indemnity and critical illness coverage.

92% of employers have taken, or are planning to take, steps to provide more, “flexible work options to align to a new way of working.”

20% of employers are considering implementing, “New messaging to help employees consider how the pandemic might affect their usual benefit choices.”

If you are unsure about the potential need to make changes to your 2021 health benefit program due to the pandemic, you are not alone. Nearly 50% of companies surveyed indicated that they are not sure about what changes they’ll make in 2021 and they are currently monitoring the situation.

Of course, many of the trends listed above have associated implementation costs. On the other hand, these benefits are designed to improve employee health, which should drive down costs in the future. Research has shown that employers are extremely concerned with the mental health of employees during the pandemic. By reading the list above, and by reading more closely into the Mercer survey, it’s clear there are significant changes in the industry that are designed to help employees maintain their mental health.

The exact extent to which these industry trends will drive down costs is yet to be determined, but companies should be aware of these trends and consider implementing them if it makes the most sense for their business model and employee population.

Communicating Your Plan Changes with Employees

Regardless of what benefits decisions your company makes for 2021 and beyond, the need to communicate openly and frequently with your employees about their benefits options has never been more important. Employees deserve to be kept in the loop about the challenges that your company is likely facing. Doing so will help company leadership maintain the trust of employees, with is critically important during these difficult times.

Your company should have a designated employee, or team of designated employees, to plan the employee communications that go along with any benefits decisions. They should constantly be asking themselves, “If we change or eliminate X benefit, how will we appropriately communicate that to our employees?” Now, more than ever before, it is critical for employees to understand their benefits. Therefore, it is more important now than ever to master the art of communicating benefits changes to your employees openly and frequently.

Even better yet, working with a proactive benefits broker that takes on the employee communication piece of your plan rollout can be even more impactful. The right benefits broker will be able to help your employees see the true value in the benefits being offered, and can help employees select the plan that’s right for them and their family.

Key Takeaways

Nearly half of companies are unsure about what difficult benefits decisions they will have to make over the next few months. Hopefully, this article has provided useful information to you as an employer or HR professional to help you be better situated to make these tough decisions.

Here are some key takeaways from this post:

Business leaders should not get deceived over the fact that their health care costs have been low during 2020. They will most likely increase substantially in 2021.

Current industry trends indicate that companies are taking precautions to limit COVID-19 outbreaks at their workplaces. Companies are also taking extra steps to care for the mental health of their employees. Voluntary benefits options are also being expanded to fill in potential gaps that may be created by upcoming plan decisions.

Employers should openly and frequently communicate with their employees about the challenging benefits decisions that may be taking place soon. Good communication is critical for maintaining positive relationships with employees, which matters now more than ever before.

The ongoing COVID-19 pandemic has created a new dynamic within the US healthcare system, leading to increased healthcare costs being passed onto employers. During this economically challenging time, it’s more important than ever before that employers are strategically managing and addressing rising healthcare costs.

There are three variable factors directly impacting healthcare costs: unit price of healthcare services, the number of services required, and the number of patients requiring service. In order to impact this equation, there are three strategies employers can deploy.

Change the unit cost of healthcare. Even prior to COVID, ineffective and uninformed healthcare decisions were already a leading cause of rising healthcare costs. Now, in a post-COVID world, the impact of poor healthcare decisions is having an even more significant impact on employers. This issue typically arises when employees lack the guidance, resources, and other information they need to make smart healthcare choices. This results in employees incurring higher costs of care and leveraging lower quality providers. These costs are then passed onto their employer. In order to combat this, employers must work with a hands-on broker that provides their employees with guidance during the benefits selection process. Additionally, the correct broker should provide employees support in selecting the best healthcare providers for their unique situation and life stage. By making more informed decisions, patients receive better healthcare outcomes and less costs are passed onto the employer.

Impact the number of services used. As the demand for routine and preventive healthcare services skyrockets in a post-COVID world, the ability for patients to receive the care they need, how and where they need it, has become increasingly important. Employees are more commonly demanding personalized guidance in managing their health. As an employer, implementing solutions that cater to employees’ unique situations or communication preferences can ensure they receive correct, accurate information that is relevant to them. Providing personalized content in easy-to-access channels helps employees proactively find care and identify other programs offered to them, such as telemedicine. As an employer, consider solutions that remove barriers to care as an important component of your overall cost-control strategy.

Manage the demand for care. The last recommended strategy is to proactively manage the number of people on your employer-sponsored healthcare plans. Each year, employers unknowingly spend millions on dependents that do not meet eligibility requirements for the benefits the company offers. By leveraging effective processes and strategies to eliminate ineligible users from their plans, companies can reduce healthcare costs. A key recommendation is to conduct a regular ineligibility audit to ensure your employee population and plans are managed in a consistent and fair manner to ensure equal treatment of employees to manage employer costs.

Are you interested in implementing these strategies at your business? Launchways can help, get in touch with us today.

This post continues our ongoing series of articles on how COVID will impact employer healthcare costs. In today’s blog, we’ll discuss four ways that COVID will likely lead to increased costs for employers.

As healthcare providers begin to reopen and quarantines are lifted, routine treatments will be significantly more expensive in a post-COVID world. During the COVID pandemic, hundreds of thousands of routine visits and procedures were delayed. As healthcare providers reopen, there will be a large surge in demand for simple procedures and medical imaging. Under normal circumstances, dedicated imaging centers and surgery centers would be the most cost-effective locations for individuals to receive the care they need. However, the large surge in demand will push many people into hospital settings to receive the testing and treatment they need. Unfortunately, in hospital settings, healthcare costs can double, triple, or even potential quadruple depending on the nature of the procedures.

During COVID, access to prescriptions has impacted the healthcare outcomes of those with chronic conditions. Under normal circumstances, individuals on long-term maintenance medications typically have access to 30-day supplies. During the COVID outbreak, many individuals with pre-existing conditions felt uncomfortable leaving their homes to refill prescriptions, leading to lower adherence rates to prescription regimens. In fact, recent research indicates that as much as one third of Americans avoided receiving necessary care due to fear of contracting COVID. When individuals with chronic conditions aren’t connected to care, this can mean substantial costs being passed onto employers. Non-adhering diabetics can cost an extra $5,000 per year. And individuals who forego mental health medications can cost an extra $10,000-$15,000.

Delays in treatments for those with chronic pain may lead to substantial treatment costs for opioid addictions. Every day, thousands of individuals undergo musculoskeletal treatments for elective procedures to reduce or eliminate chronic pain. However, due to COVID, all of those procedures were delayed. In non-COVID times, these individuals would be able to seek other forms of care, such as physical therapy, to help manage that pain while waiting for corrective surgery. However, during COVID individuals were also unable to access these treatment options. Many frustrated patients turned to their doctors for pain medication to help manage pain during surgery delays. These unfortunate circumstances may very well likely lead to future costs due to opioid dependency. Generally speaking, the ongoing opioid crisis costs the U.S. roughly $78.5 billion each year. And research estimates that opioid addiction costs $14,000 in direct claims costs per patient per year.

Delayed preventative care creates future risks for more serious conditions and costly treatment plans. In many cases, preventative screenings and treatments are crucial for limiting the amount of critical care individuals need. During non-COVID times, cancer screenings were rising in frequency and are generally recommended by providers. In the case of most treatable cancers, such as breast cancer or colon cancer, early detection is the best strategy to limit complications and ensure positive patient outcomes. Unfortunately, during COVID-19, preventative care and screenings were halted for several months. These delays are likely to lead to substantially more serious diagnoses that are harder to treat and more expensive to provide care for.